In this post, we discuss:

- History of Accounting

- Double Entry System

- Modern Bookkeeping

- Conclusion

History of Accounting

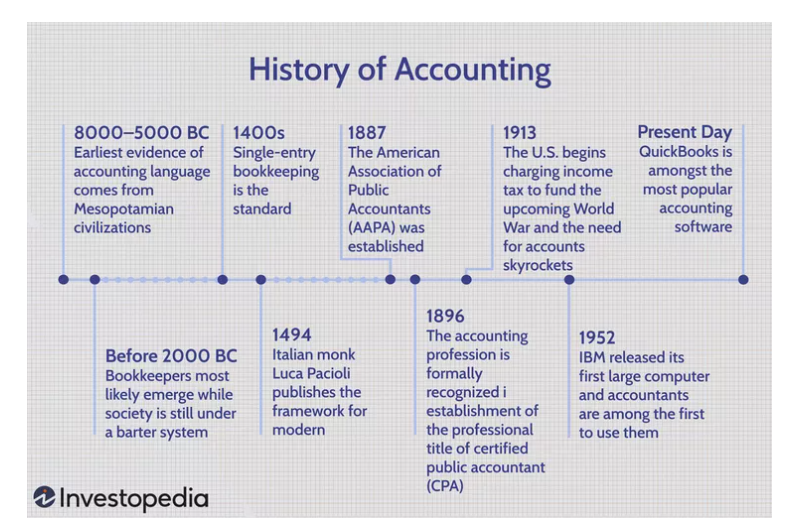

Being in a profession for over 20 years now, I am still fascinated about the origin of accounting as a subject, how did it came to light , who and when began the first ever thought of a process to record transactions.

The earliest evidence as per Investopedia goes back to around 7000 BC and to the Sumerian civilizations , who used clay tablets to record trades while being one of the largest hubs at that time.

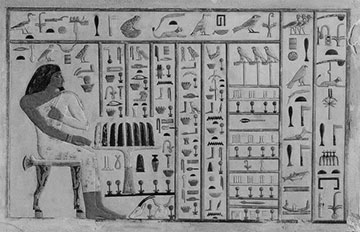

See Ancient Egypt table from around 7500 BC, the clay tablet became more sophisticated and complex with time, used as tokens of payments or receipts. It is not known if there was monetary system, however the clay tabs were widely used by farmers or receipt for completed tasks paid by Pharaoh.

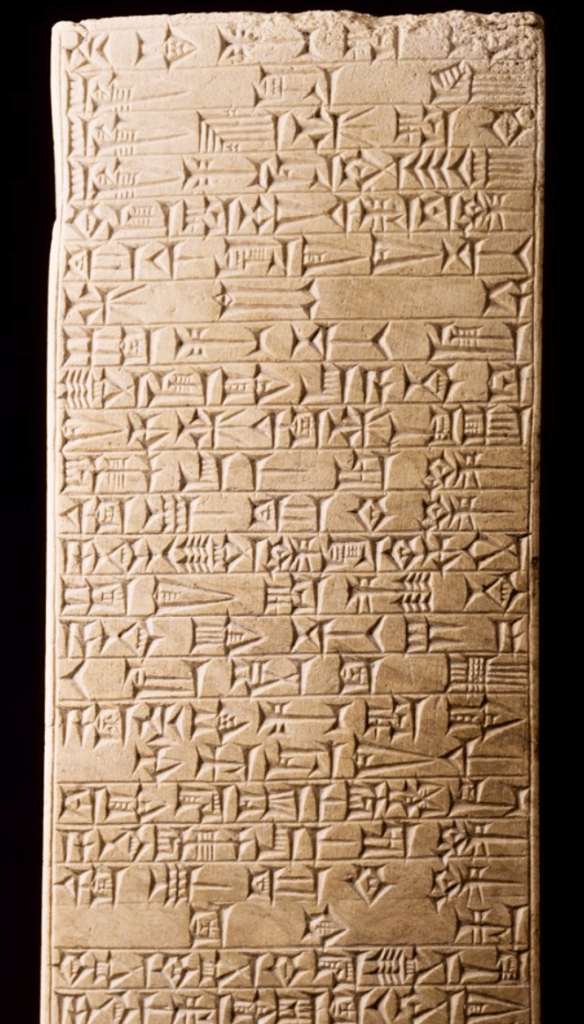

The accountants were responsible not only record the transactions, but also for tax computation with Abacus and records maintenance on Papyrus paper. The significant example of such is the record of wealth for King Hammurabi:

The real origins of Abacus still remain unknown, some sources claim China and others – Mesopotamia, Egypt, Greece. However, the earliest mentioning of the Abacus was around 2700 BC in Mesopotamia.

History of Double Entry System

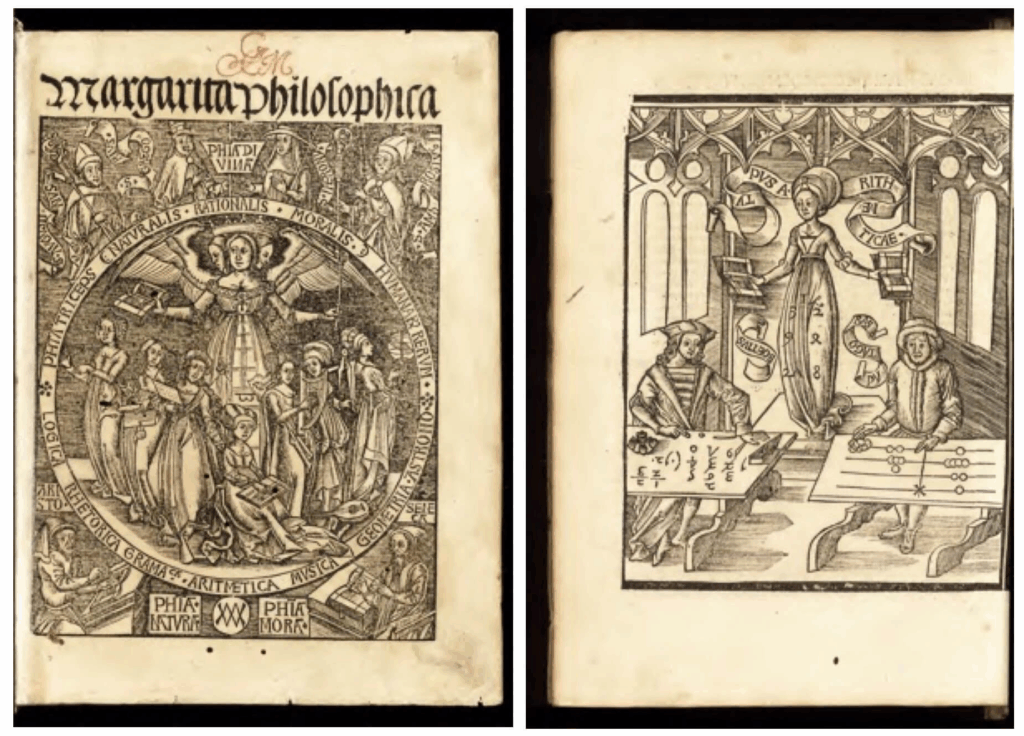

All the way up to 15th century, bookkeeping was not well organized, until “Everything About Arithmetic, Geometry, and Proportion” a first published work was written by Italian mathematician Luca Pacioli in ca 1494. The most important idea was based around double entry system and expanding what has already been discussed in 1458 manuscript “Of Trading and the Perfect Trader” by merchant and humanist – Benedetto Cotrugli.

Still Luca Pacioli is known as ‘Father of Accounting’ as his work lead to widespread of the double entry concept and bookkeeping. He was also a math teacher and a close friend of Leonardo Da Vinci.

The double entry system is used in bookkeeping and means that every transaction has at least two parties. In other words, sale entry would be reflected in receiving cash -thus involving two accounts, for example: Sales and Cash or exchange of an item (sale) for money (cash).

Cash vs Credit transactions

The concept of money worth comes when you buy goods from your supplier on credit with a payment later on. For example, you have bought a piece of machinery from Xerox, but your payment terms are 30 days. This transaction is “in money’s worth” and different from paying to an employee. The payment to your employee would be called “in money” or immediate payment.

A sale with 30 days credit as double entry would be in the Sales and Aged Receivables accounts. Once the customer has paid for the invoice, we use Aged Receivables and Cash accounts.

What is Modern Bookkeeping

Bookkeeping as through all of the year is still a process of recording daily financial transactions into a some sort of a bookkeeping system. The way of recording transactions can be done either on paper or in digital format. Today, the most common software systems used for bookkeeping are Xero, QuickBooks or Sage. The bookkeeping entries made ensure that funds earned as income or spent for business purposes are properly accounted for.

The bookkeeping entries are grouped into Accounts (personal, real or nominal), forming an accounting ledger called a Book of Accounts. The bookkeeper’s responsibility is to enter the transactions accurately by using the correct accounts.

Conclusion

The double-entry system plays a vital role in organizing and balancing the accounts. Thus presenting the financial information as a true and fair. The true and fair view is an accounting concept that was implemented into the UK company law in 1947.

Financial statements are expected to present a ‘true and fair’ view if they:

•comply with any relevant legislation or regulatory requirements;

•comply with accounting standards and generally accepted accounting practice (GAAP);

•provide an unbiased (fair and reasonable) presentation;

•are compiled with sufficient accuracy within the bounds of materiality; and

•faithfully represent the underlying commercial activity (the concept of ‘substance over legal form’). source

So even the smallest business should establish bookkeeping to know how much was bought or sold; was received and paid. Without such a system, it will create chaos. Using the accounting software makes the bookkeeping a much easier process. If bookkeeping tasks are done regularly; the business owners will be up to date to make better decisions. How regularly, it is will depend on the business size and number of transactions. Generally, it can be from daily to weekly tasks, with a monthly salary payments and reconciliation.

Read next:

- What Bookkeepers Do. A Typical Day.

- Business Transactions

- Sole Trader vs Partnership vs Limited Company Explained

Sources:

Record Keeping in Ancient Mesopotamia – Knowledge Based Society